Moving Average in R

07.19.2021

Intro

When working with time series, we often want to view the average over a certain number of days. For example, we can view a 7-day rolling average to give us an idea of change from week to week. In this article, we will learn how to conduct a moving average in R.

Data

Let’s load a data set of monthly milk production. We will load it from the url below. The data consists of monthly intervals and kilograms of milk produced.

df <- read.csv('https://raw.githubusercontent.com/ourcodingclub/CC-time-series/master/monthly_milk.csv')

df$month = as.Date(df$month)

head(df)## month milk_prod_per_cow_kg

## 1 1962-01-01 265.05

## 2 1962-02-01 252.45

## 3 1962-03-01 288.00

## 4 1962-04-01 295.20

## 5 1962-05-01 327.15

## 6 1962-06-01 313.65Now, we convert our data to a time series object then to an zoo object

to have access to many indexing methods explored below.

library(zoo)##

## Attaching package: 'zoo'

## The following objects are masked from 'package:base':

##

## as.Date, as.Date.numericdf.ts = ts(df[, -1], frequency = 12, start=c(1962, 1, 1))

df.ts = as.zoo(df.ts)

head(df.ts)## Jan 1962 Feb 1962 Mar 1962 Apr 1962 May 1962 Jun 1962

## 265.05 252.45 288.00 295.20 327.15 313.65Conducting a moving average

To conduct a moving average, we can use the rollapply function from

the zoo package. This function takes three variables: the time series,

the number of days to apply, and the function to apply. In the example

below, we run a 2-day mean (or 2 day avg).

library(zoo)

ts.2day.mean = rollapply(df.ts, 2, mean)

head(ts.2day.mean)## Jan 1962 Feb 1962 Mar 1962 Apr 1962 May 1962 Jun 1962

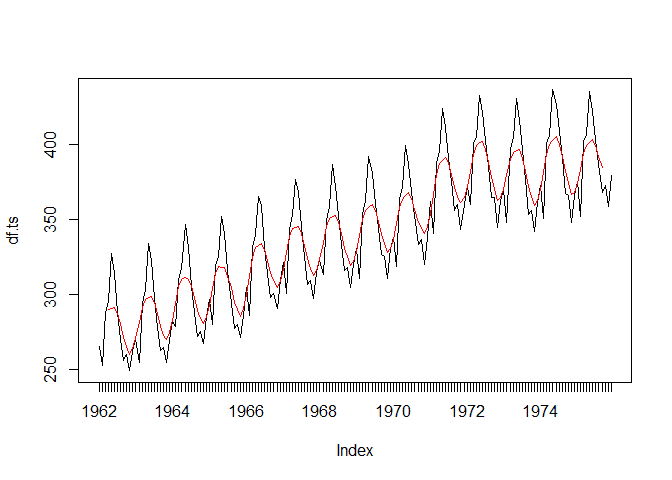

## 258.750 270.225 291.600 311.175 320.400 300.825We can also plot the data over our orignal time series to see how the avg smoothed out the data.

plot(df.ts)

lines(ts.2day.mean, col = 'red')

Let’s do another example with a 7-day avg which is a common task in disease outbreaks and stocks.

ts.7day.mean = rollapply(df.ts, 7, mean)

head(ts.7day.mean)## Apr 1962 May 1962 Jun 1962 Jul 1962 Aug 1962 Sep 1962

## 289.9286 290.5714 291.0214 286.9714 280.3500 271.0286Again, let’s plot the data.

plot(df.ts)

lines(ts.7day.mean, col = 'red')

Other Rolling Functions

You may have noticed from the above that we can do more than a rolling

average with the rollapply function. We can actually apply any math

function. Let’s run a couple of more examples, sum and median.

ts.7day.median = rollapply(df.ts, 7, median)

head(ts.7day.median)## Apr 1962 May 1962 Jun 1962 Jul 1962 Aug 1962 Sep 1962

## 288.00 288.00 288.00 288.00 269.55 261.90ts.7day.sum = rollapply(df.ts, 7, sum)

head(ts.7day.sum)## Apr 1962 May 1962 Jun 1962 Jul 1962 Aug 1962 Sep 1962

## 2029.50 2034.00 2037.15 2008.80 1962.45 1897.20