PCA Regression in R

06.18.2021

Intro

PCA or Principal component regression is the process of using PCA to preprocess the data then running a linear regression model. The PCA process will give us new variables or predictors that we can use in modeling. In this article, we will learn how to use pca regression in R.

Data

For this tutorial, we will use the Boston data set which includes

housing data with features of the houses and their prices. We would like

to predict the medv column or the medium value.

library(MASS)

data(Boston)

str(Boston)## 'data.frame': 506 obs. of 14 variables:

## $ crim : num 0.00632 0.02731 0.02729 0.03237 0.06905 ...

## $ zn : num 18 0 0 0 0 0 12.5 12.5 12.5 12.5 ...

## $ indus : num 2.31 7.07 7.07 2.18 2.18 2.18 7.87 7.87 7.87 7.87 ...

## $ chas : int 0 0 0 0 0 0 0 0 0 0 ...

## $ nox : num 0.538 0.469 0.469 0.458 0.458 0.458 0.524 0.524 0.524 0.524 ...

## $ rm : num 6.58 6.42 7.18 7 7.15 ...

## $ age : num 65.2 78.9 61.1 45.8 54.2 58.7 66.6 96.1 100 85.9 ...

## $ dis : num 4.09 4.97 4.97 6.06 6.06 ...

## $ rad : int 1 2 2 3 3 3 5 5 5 5 ...

## $ tax : num 296 242 242 222 222 222 311 311 311 311 ...

## $ ptratio: num 15.3 17.8 17.8 18.7 18.7 18.7 15.2 15.2 15.2 15.2 ...

## $ black : num 397 397 393 395 397 ...

## $ lstat : num 4.98 9.14 4.03 2.94 5.33 ...

## $ medv : num 24 21.6 34.7 33.4 36.2 28.7 22.9 27.1 16.5 18.9 ...Basic PCA Regression in R

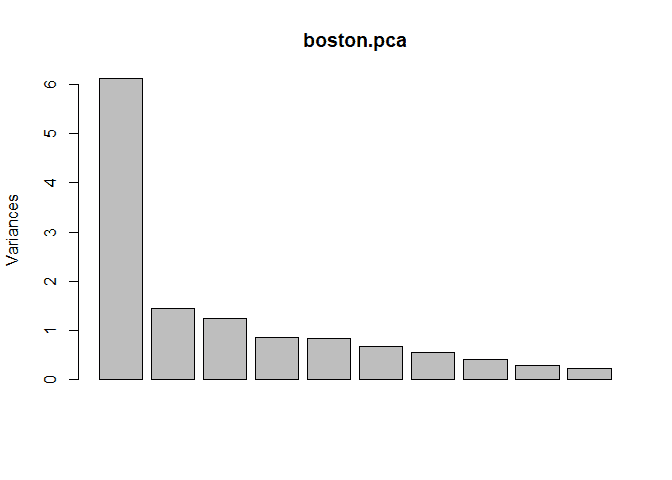

To run pca in R, we can use the built in prcomp function. This will

return new variables that are linear combinations of our predictors. We

can plot this return to see how much of the variance of our data is

examplained by each new predictor.

boston.preds <- subset(Boston, select=-c(medv))

boston.pca <- prcomp(boston.preds, center = TRUE, scale = TRUE)

plot(boston.pca)

To create a pca regression model, we can use the pcr method from the

pls package similar to how we run a lm. We pass the model equation,

the data set, and we set scale to True so our data will be scaled before

building a model.

library(pls)## Warning: package 'pls' was built under R version 4.0.5

##

## Attaching package: 'pls'

## The following object is masked from 'package:stats':

##

## loadingsmodel = pcr(medv ~ ., data = Boston, scale = TRUE)

summary(model)## Data: X dimension: 506 13

## Y dimension: 506 1

## Fit method: svdpc

## Number of components considered: 13

## TRAINING: % variance explained

## 1 comps 2 comps 3 comps 4 comps 5 comps 6 comps 7 comps 8 comps

## X 47.13 58.15 67.71 74.31 80.73 85.79 89.91 92.95

## medv 37.42 45.59 63.59 64.78 69.70 70.05 70.05 70.56

## 9 comps 10 comps 11 comps 12 comps 13 comps

## X 95.08 96.78 98.21 99.51 100.00

## medv 70.57 70.89 71.30 73.21 74.06Modeling PCA Regression in R with Caret

We will now see how to model a pca regression using the Caret package.

We will use this library as it provides us with many features for real

life modeling.

To do this, we use the train method. We pass the same parameters as

above, but in addition we pass the method = 'lm' model to tell Caret

to use a linear model.

As stated before, pca is actually just a processing step. We can pass

preProcess = c("pca") to the train method to build a pca model.

library(caret)## Loading required package: lattice

## Loading required package: ggplot2

##

## Attaching package: 'caret'

## The following object is masked from 'package:pls':

##

## R2set.seed(1)

model <- train(

medv ~ .,

data = Boston,

method = 'lm',

preProcess = c("pca")

)

model## Linear Regression

##

## 506 samples

## 13 predictor

##

## Pre-processing: principal component signal extraction (13), centered

## (13), scaled (13)

## Resampling: Bootstrapped (25 reps)

## Summary of sample sizes: 506, 506, 506, 506, 506, 506, ...

## Resampling results:

##

## RMSE Rsquared MAE

## 5.119009 0.6897642 3.490649

##

## Tuning parameter 'intercept' was held constant at a value of TRUEWe could use summary again to get extra details. We also see that our

RMSE is 5.119009 and our Rsquared is 0.6897642.

Preprocessing with Caret

One feature that we use from Caret is preprocessing. Often in real life

data science we want to run some pre processing before modeling. We will

center and scale our data by passing the following to the train method:

preProcess = c("center", "scale").

set.seed(1)

model2 <- train(

medv ~ .,

data = Boston,

method = 'lm',

preProcess = c("center", "scale", "pca")

)

model2## Linear Regression

##

## 506 samples

## 13 predictor

##

## Pre-processing: centered (13), scaled (13), principal component

## signal extraction (13)

## Resampling: Bootstrapped (25 reps)

## Summary of sample sizes: 506, 506, 506, 506, 506, 506, ...

## Resampling results:

##

## RMSE Rsquared MAE

## 5.119009 0.6897642 3.490649

##

## Tuning parameter 'intercept' was held constant at a value of TRUESplitting the Data Set

Often when we are modeling, we want to split our data into a train and

test set. This way, we can check for overfitting. We can use the

createDataPartition method to do this. In this example, we use the

target medv to split into an 80/20 split, p = .80.

This function will return indexes that contains 80% of the data that we should use for training. We then use the indexes to get our training data from the data set.

set.seed(1)

inTraining <- createDataPartition(Boston$medv, p = .80, list = FALSE)

training <- Boston[inTraining,]

testing <- Boston[-inTraining,]We can then fit our model again using only the training data.

set.seed(1)

model3 <- train(

medv ~ .,

data = training,

method = 'lm',

preProcess = c("center", "scale", "pca")

)

model3## Linear Regression

##

## 407 samples

## 13 predictor

##

## Pre-processing: centered (13), scaled (13), principal component

## signal extraction (13)

## Resampling: Bootstrapped (25 reps)

## Summary of sample sizes: 407, 407, 407, 407, 407, 407, ...

## Resampling results:

##

## RMSE Rsquared MAE

## 5.160234 0.6852131 3.540184

##

## Tuning parameter 'intercept' was held constant at a value of TRUENow, we want to check our data on the test set. We can use the subset

method to get the features and test target. We then use the predict

method passing in our model from above and the test features.

Finally, we calculate the RMSE and r2 to compare to the model above.

test.features = subset(testing, select=-c(medv))

test.target = subset(testing, select=medv)[,1]

predictions = predict(model3, newdata = test.features)

# RMSE

sqrt(mean((test.target - predictions)^2))## [1] 5.343331# R2

cor(test.target, predictions) ^ 2## [1] 0.6865547Cross Validation

In practice, we don’t normal build our data in on training set. It is

common to use a data partitioning strategy like k-fold cross-validation

that resamples and splits our data many times. We then train the model

on these samples and pick the best model. Caret makes this easy with the

trainControl method.

We will use 10-fold cross-validation in this tutorial. To do this we

need to pass three parameters method = "repeatedcv", number = 10

(for 10-fold). We store this result in a variable.

set.seed(1)

ctrl <- trainControl(

method = "cv",

number = 10,

)Now, we can retrain our model and pass the trainControl response to

the trControl parameter. Notice the our call has added

trControl = set.seed.

set.seed(1)

model4 <- train(

medv ~ .,

data = training,

method = 'lm',

preProcess = c("center", "scale", "pca"),

trControl = ctrl

)

model4## Linear Regression

##

## 407 samples

## 13 predictor

##

## Pre-processing: centered (13), scaled (13), principal component

## signal extraction (13)

## Resampling: Cross-Validated (10 fold)

## Summary of sample sizes: 367, 366, 367, 366, 365, 367, ...

## Resampling results:

##

## RMSE Rsquared MAE

## 4.980723 0.7122785 3.550651

##

## Tuning parameter 'intercept' was held constant at a value of TRUEThis results seemed to have improved our accuracy for our training data. Let’s check this on the test data to see the results.

test.features = subset(testing, select=-c(medv))

test.target = subset(testing, select=medv)[,1]

predictions = predict(model4, newdata = test.features)

# RMSE

sqrt(mean((test.target - predictions)^2))## [1] 5.343331# R2

cor(test.target, predictions) ^ 2## [1] 0.6865547Tuning Hyper Parameters

We can also use caret to tune hyper parameters in models. PCA Regression doesn’t have any, so we don’t need to tune the model.